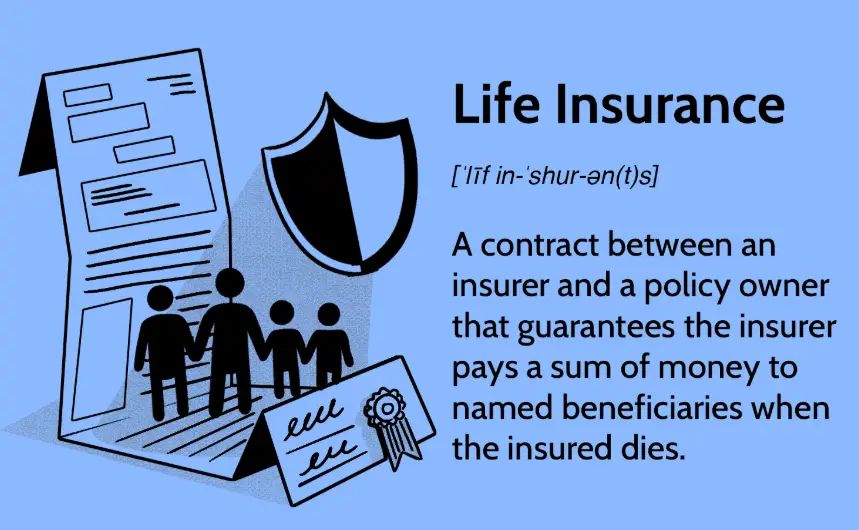

Life Insurance Policy: Life is unpredictable. While we cannot control what happens tomorrow, we can prepare for it. One of the smartest financial decisions anyone can make is securing a Life Insurance Policy. Yet, many people either misunderstand life insurance or postpone buying it until it’s too late.

This comprehensive guide explains everything you need to know about life insurance policies—from what they are and how they work, to the different types, benefits, costs, and how to choose the right one for your needs.

Whether you’re a first-time buyer or simply looking to understand life insurance better, this guide has you covered.

ALSO READ: GoFundMe Account Creation | See Full Guidelines

What Is a Life Insurance Policy?

A Life Insurance Policy is a legal contract between an individual (the policyholder) and an insurance company. In exchange for regular payments known as premiums, the insurer promises to pay a death benefit to the policyholder’s chosen beneficiaries when the insured person dies.

The primary purpose of life insurance is financial protection. It ensures that your loved ones are not left struggling financially in the event of your death.

Key Parties Involved

- Policyholder – The person who owns the policy

- Insured – The person whose life is covered

- Beneficiary – The person(s) who receive the payout

- Insurer – The insurance company

Why Life Insurance Policy Is Important

Life insurance is not just for the elderly or wealthy. It is essential for anyone with financial responsibilities.

Major Benefits of a Life Insurance

- Provides financial security for dependents

- Covers funeral and burial expenses

- Replaces lost income

- Pays off debts and loans

- Helps fund children’s education

- Offers tax benefits (in many countries)

- Supports long-term financial planning

Without life insurance, families may be forced to sell assets, take loans, or drastically change their lifestyle after the loss of a breadwinner.

How Does Life Insurance Work?

Life insurance works on a simple principle:

- You choose a policy and coverage amount

- You pay premiums (monthly, quarterly, or annually)

- The policy remains active as long as premiums are paid

- When the insured dies, the insurer pays the death benefit to beneficiaries

Some policies also include savings or investment components, allowing you to build cash value over time.

ALSO READ: Online Businesses You Can Start Today With Little or No Money

Types of Life Insurance Policies

There are two main categories of life insurance: Term Life Insurance and Permanent Life Insurance.

1. Term Life Insurance

Term life insurance provides coverage for a specific period—usually 10, 20, or 30 years.

Features

- Fixed coverage period

- Lower premiums

- No cash value

- Pays out only if death occurs during the term

Pros

- Affordable

- Simple to understand

- Ideal for young families and income earners

Cons

- No payout if the policy expires

- Premiums increase upon renewal

Best For: People seeking affordable protection for a specific financial responsibility, such as a mortgage or child education.

2. Whole Life Insurance

Whole life insurance provides lifetime coverage and includes a cash value component.

Features

- Lifetime protection

- Fixed premiums

- Guaranteed death benefit

- Builds cash value

Pros

- Never expires

- Acts as a savings tool

- Cash value can be borrowed

Cons

- Higher premiums

- Less flexibility

Best For: Long-term financial planning and estate protection.

3. Universal Life Insurance

Universal life insurance combines lifetime coverage with flexible premiums and savings.

Features

- Adjustable premiums

- Flexible death benefit

- Accumulates interest

Pros

- Customizable

- Investment growth potential

Cons

- Complex

- Cash value not guaranteed

4. Endowment Life Insurance

Endowment policies pay a lump sum either on death or after a specified maturity period.

Key Benefits

- Savings + protection

- Ideal for future goals

- Guaranteed payout

5. Group Life Insurance

Provided by employers to employees, usually at low or no cost.

Limitations

- Coverage ends when employment ends

- Usually insufficient on its own

Life Insurance Riders (Add-Ons)

Riders enhance your policy’s coverage. Common riders include:

- Accidental Death Benefit Rider

- Critical Illness Rider

- Waiver of Premium Rider

- Disability Income Rider

Adding riders increases premium costs but provides broader protection.

Who Needs a Life Insurance?

Life insurance is important if you:

- Are married

- Have children

- Support aging parents

- Own a business

- Have outstanding debts

- Want estate planning benefits

Even single individuals can benefit, especially if they have dependents or financial obligations.

How Much Life Insurance Coverage Do You Need?

A common rule is 10–15 times your annual income, but this varies based on:

- Current income

- Outstanding debts

- Family size

- Lifestyle expenses

- Future financial goals

Coverage Calculation Example

If you earn ₦3,000,000 annually:

- Recommended coverage: ₦30–45 million

Factors Affecting Life Insurance Premiums

Life insurance premiums are determined by several factors:

- Age

- Gender

- Health condition

- Lifestyle habits (smoking, alcohol)

- Occupation

- Coverage amount

- Policy duration

The younger and healthier you are, the cheaper your premiums will be.

Life Insurance and Taxes

In many countries:

- Premiums may be tax-deductible

- Death benefits are tax-free

- Cash value grows tax-deferred

Always consult a financial advisor or tax professional for local regulations.

Common Life Insurance Myths

Myth 1: Life insurance is only for old people

Truth: Younger people get cheaper premiums.

Myth 2: It’s too expensive

Truth: Term policies are very affordable.

Myth 3: I don’t need it because I’m single

Truth: Debts and dependents still matter.

READ ALSO: PayPal Account Creation | See Full Guidelines

How to Choose the Right Life Insurance

When selecting a policy, consider:

- Your financial goals

- Number of dependents

- Budget

- Coverage duration

- Type of policy

- Insurance company reputation

Checklist Before Buying

- Compare multiple insurers

- Read policy terms carefully

- Understand exclusions

- Ask about claim settlement ratio

When Is the Best Time to Buy Life Insurance?

The best time to buy life insurance is now.

Buying early:

- Locks in lower premiums

- Provides longer coverage

- Ensures financial security sooner

Delaying can result in higher premiums or denial due to health issues.

Life Insurance Claims Process

The claim process usually involves:

- Notifying the insurer

- Submitting required documents

- Verification

- Claim settlement

Important documents include:

- Death certificate

- Policy document

- Claim form

- Beneficiary ID

Life Insurance vs Health Insurance

| Feature | Life Insurance | Health Insurance |

|---|---|---|

| Covers | Death | Medical expenses |

| Duration | Long-term | Annual |

| Purpose | Financial protection | Healthcare costs |

Both are essential and serve different purposes.

Life Insurance as a Financial Planning Tool

Life insurance is more than protection—it’s a strategic financial asset:

- Retirement planning

- Wealth transfer

- Estate planning

- Loan collateral

Permanent life policies can be leveraged to build long-term wealth.

Mistakes to Avoid When Buying Life Insurance

- Buying insufficient coverage

- Ignoring policy exclusions

- Choosing based on price alone

- Not disclosing medical history

- Forgetting to update beneficiaries

Conclusion

A life insurance policy is one of the most powerful tools for securing your family’s future. It provides peace of mind, financial stability, and long-term protection against life’s uncertainties.

Whether you choose term, whole, or universal life insurance, the most important step is taking action. The right policy today can protect your loved ones for decades to come.

Life insurance isn’t about preparing for death—it’s about protecting life.

Pingback: Life Insurance Companies In Nigeria | Best Ones To Go For - GISTWAVESMEDIA.COM